The minivan crests yet another hill. The sun is setting. The van descends the gently rolling hill that ends once again in a cul-de-sac.

"Didn’t we do this street already?" Harold Folley, an apprentice organizer with the Virginia Organizing Project, leans back from the wheel for a second look at the seemingly endless rows of beige houses for a better look. No, it turns out, they haven’t, though the neighborhood’s near-aesthetic conformity makes it hard to tell.

After knocking on 60 or 70 doors and handing out fliers on payday lending, Virginia Organizing Project canvassers consider it a success if they can get six people to call their elected officials |

Harold parks on the curb. Three doors open and the van disgorges itself. Harold, two VOP interns and a volunteer take a quick look around, clipboards in hand. It’s nearly 8pm and just over 90 degrees. They’ve been canvassing the Mill Creek neighborhood for almost two hours.

Harold walks up to one of the front doors and rings the bell. A man answers, and Harold begin his pitch. After offering to recycle printer cartridges or cell phones—a good icebreaker, Harold admits—he gets to the meat of the conversation.

"Are you familiar with payday loans?"

The man rubs his gray mustache. Sure, he says. He’s one of the few the VOP team talks to today who is.

"What do you think about those companies?" Harold asks, leaning in.

"Well," the man says, pausing to consider. "I think when [the Virginia legislature] was going to control them, they made a mistake in not doing so."

"Oh man!" says Harold, flashing a grin below a straw hat that can only be described as Crocodile Dundee chic. "So you do know about them."

Since May, VOP has been going door to door, educating residents about predatory lending, specifically payday loans. There’s no credit check. All that’s needed is a job and a personal check made out to the lender for the loan amount, plus $15 for every $100 borrowed, per week.

Getting just one of these loans more often than not leads to a vicious cycle. When the borrower’s paycheck comes, he or she often can’t repay the loan and pay regular bills, too. How do you cover the difference? Another payday loan.

"A lot of people don’t know about these loans," says Harold. "It’s so amazing, because you can go to the inner-city, low-income areas and they know all about payday loans."

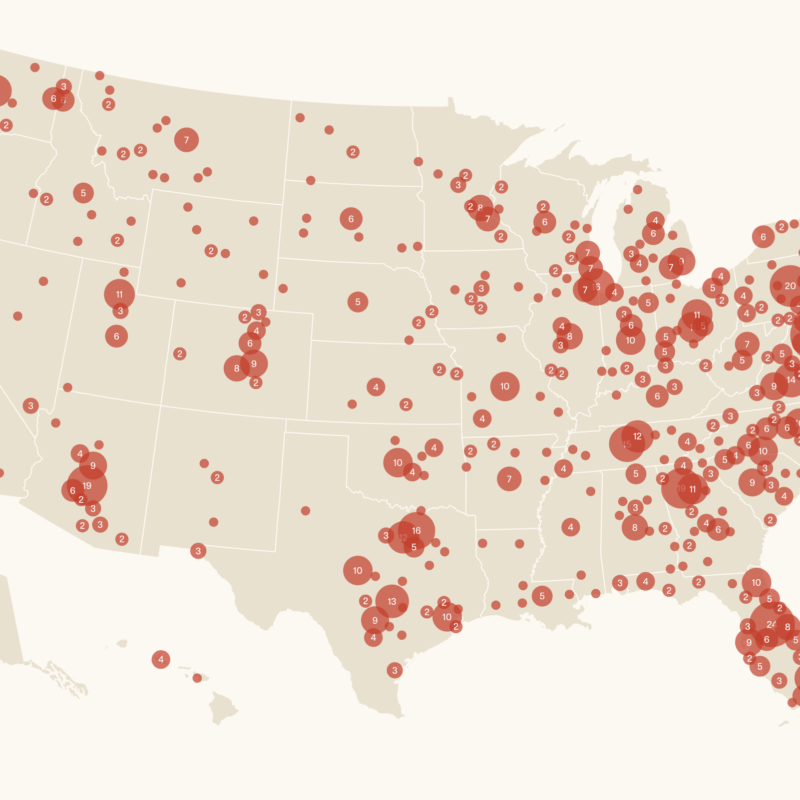

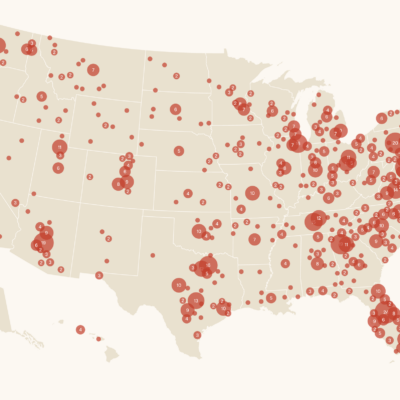

While states like Maryland, West Virginia and North Carolina have all passed legislation prohibiting payday loans, in 2002 the Virginia General Assembly passed legislation allowing them. Last year several bills attempting to stop or cap the annual percentage rate (APR) on payday loans died in the Virginia House. According to a California State University of Northridge study, Virginia has 743 payday lenders. It has 382 McDonald’s.

VOP intern Sarah Sievert, an American Studies major at UVA, steps onto yet another porch and rings the bell. A youngish man opens the door. He’s got the start of a red handlebar mustache, the ends just beginning to curl. He gives Sarah a polite smile. His t-shirt reads RIT Intramural Muff Diving Team.

If Sarah sees the t-shirt, she doesn’t show it. She jumps into her pitch. Do you know about predatory lending? A polite no. Sarah gives him a flyer and breaks it down: the 391-percent APR, the cycle of debt they perpetuate. The man, looking concerned, takes the flyer. Sarah points to the contact information for Rob Bell and Creigh Deeds, and urges him to call or write the delegate and state senator as a part of the campaign to cap the APR of these loans at 36 percent.

"Some people do get really fired up," says Sarah. "They’re super gung-ho and like ‘I’m going to do something!’ And I totally believe them. Most are kind of like him, where I just think they’re being polite."

The temperature’s around 90 degrees, and the canvassers start to drag a little, hair slick with sweat. The sun’s almost down, and Harold wants to call it a night. But Kevin Simowitz, intern and fellow UVA American studies major, scoffs. There’s still more to do.

"I can be at a house for 10 or 15 minutes, and that helps," says Kevin. "Because the only way you win social justice issues is by building relationships."

A couple minutes later, a different connection is made. A man tells Harold that soliciting is prohibited in the neighborhood. He might call the cops. The crew piles in the van and drives by the anti-solicitation watchdog himself. He’s on the phone.

Harold figures they talked to 60 or 70 people today. There’s about a 10 percent chance that someone they’ve talked to will take action. After three hours of hoofing it up and down Mill Creek hills, six or seven people will probably contact Bell or Deeds.

After three hours, 90 degrees and what seems like a thousand faces, isn’t that discouraging?

"No!" Harold says. "If Creigh Deeds or Rob Bell get six or seven calls [a day] three times a week, that’s good for us. Those six or seven add up. And they’ve been adding up over the summer."

Sure, but can a handful of calls a day stand up to the 15 or so lobbyists that the lending industry sics on legislatures? Kevin points to the states that have passed legislation against the industry.

"I think about small groups of people winning victories," he says. "Last year we came really close. This became the hot-button issue. So you come back and talk to more people. People find out about injustice, and that eventually carries more weight in this state and our country than money does, even if it takes a little while."

The sun’s gone down. Kevin and Sarah ride in the van, ironing out the logistics for tomorrow’s canvassing. It’s only supposed to get hotter.

C-VILLE welcomes news tips from readers. Send them to news@c-ville.com.